- Market Overview

- Futures

- Options

- Custom Charts

- Spread Charts

- Market Heat Maps

- Historical Data

- Stocks

- Real-Time Markets

- Site Register

- Mobile Website

- Trading Calendar

- Futures 101

- Commodity Symbols

- Real-Time Quotes

- CME Resource Center

- Farmer's Almanac

- USDA Reports

Weaker US jobs report and US dollar shift outlook

Howdy market watchers!

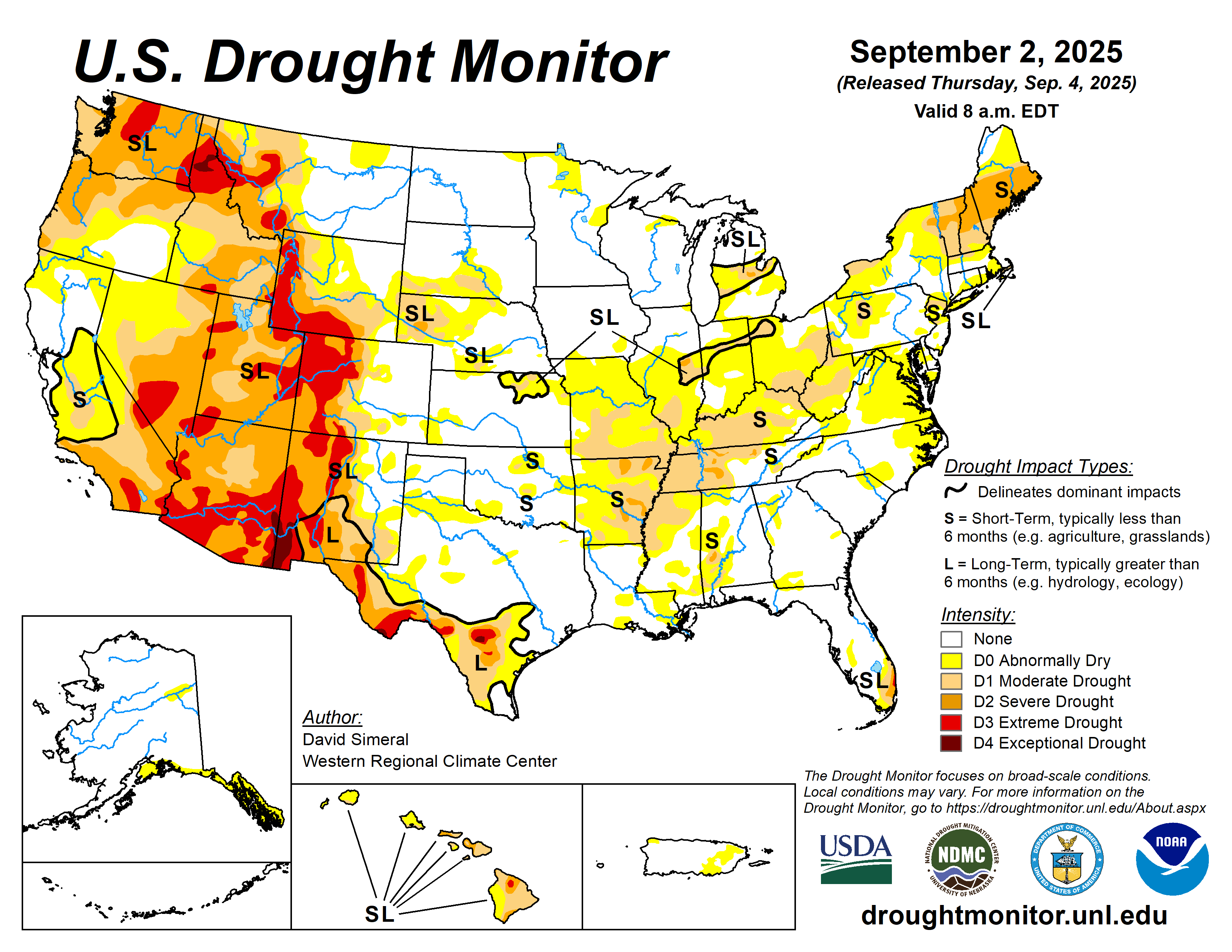

The start of September means we are in the final countdown of the 3rd quarter of 2025, already! That means summer is unofficially over and we are back to the grind. In Oklahoma, it has been difficult for farmers to do much of anything recently with continuous rain falling across the area. Coverage, however, has been spotty with drought re-emerging across several states across the Midwest and South.

Corn harvest is progressing, but continues to be paused by showers and overcast conditions. I was in southern Missouri on Thursday and they are experiencing D1 drought conditions in stark contrast to conditions further west where volunteer wheat and weeds are carpeting fields right ahead of the start to winter wheat planting.

Wheat Streak Mosaic Virus was a major issue across Kansas this past year and with all the volunteer wheat, I fear we may see much more of this in areas that have seen heavy rainfall, which have been ideal conditions for the wheat curl mite that spread this pathogenic virus. When making your seed wheat decision if planting early this year, it may be prudent to select a variety with tolerance to Wheat Streak Mosaic Virus. Army worms are also thick with the constant green vegetation from wet conditions bridging their life cycle to early wheat planting. Apply insecticide seed treatment to your seed wheat for control post-emergence. It should prevent you from having to spray multiple times for army worms or having to replant altogether. Sidwell Seed has a wide selection of varieties with Wheat Streak Mosaic Virus tolerance as well as seed treatment capabilities to protect your investment and maximize fall forage as well as grain yield.

It is sure hard to get overly excited about planting wheat for grain only at these price levels. In fact, I believe we will see reduced wheat acres planted this year and of those, increased graze out acres. However, the cure for lower prices is lower prices and so we will have to see how global demand and supply evolve over this next marketing year. Europe’s wheat crop production and export estimates have been inching higher in recent weeks as has Russia’s expectations.

It seems the supply side will not be a constraint despite recent revisions lower of world ending stocks in USDA’s WASDE reports. The question will be demand and from where that demand will be met with tariff and logistics issues as well as fluctuations in currency values.

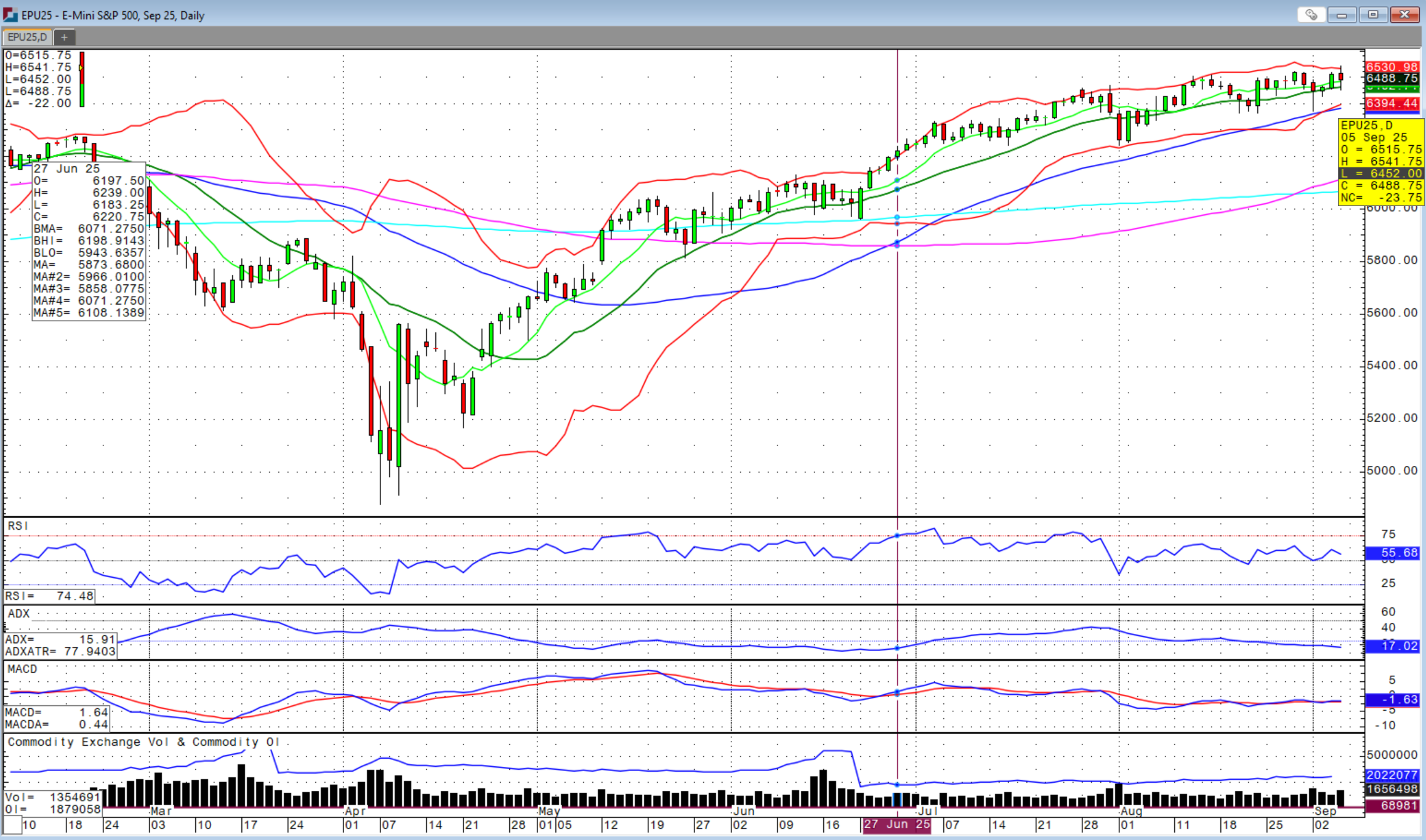

The US dollar sold off Friday to the lowest level since late July, sparked by the weaker than expected August jobs report released that morning. The Bureau of Labor Statistics (BLS) reported that just 22,000 jobs were created in August versus 75,000 jobs expected. The unemployment rate increased to 4.3 percent, but in line with expectations. While revisions up were made to the July jobs number, changes to the June number actually showed that 13,000 jobs were lost during the month instead of slight growth previously reported.

With weakening labor market data now trending, the odds of a September interest rate cut by the Federal Reserve are now 100 percent with a 12 percent likelihood that this cut could be 50 basis points instead of the widely anticipated 25 basis points. Rate cuts can be welcome news for the equity markets until the realization that it is being driven by weakness in the job market that could begin to expose broader concerns about the strength of consumer demand, the main driver of the economy.

And yet, the S&P 500 still made a new, record high on Friday, but just as the jobs report was released before selling off into the close. Now, we will have to see how this post-Labor Day demand situation evolves for the US consumer heading into the holidays.

September is often a volatile month for markets for this very reason, and it began to show in the cattle markets this week as well. We have yet to retest the August 27th high across cattle contracts with this week seeing the most weakness we’ve seen in months with feeder and live cattle contracts both closing below their 9-day moving averages and trading down near the 20-day moving averages. Having said that, the cash markets remain on fire! The sale barns continue to see incredible strength from buyers while cash fed cattle reached $242 in Texas and Kansas with some $243 reported in Kansas and a solid $243 trades in Nebraska.

Front-month October live cattle futures closed Friday around $236. What will break this market and when? Despite volatility in the futures contracts, the cash trade continues to ignore any of it, as of now. These cattle markets often peak in the 3rd quarter, which is this month and so be aware, but there are plenty of seasonal patterns that are not holding true in this current market environment.

The legal challenges to nearly every move by the Trump Administration is causing more headline risk across the economy as companies become further confused on how to move forward. With the weaker US dollar and strong new crop exports despite more old crop net cancellations this week in corn and soybeans, I feel that we could see a rally in grains, specifically corn and wheat, leading up to the September 12th USDA WASDE and Crop Production reports. We are likely to see some slight revisions lower in the US corn yield in this next report, but once that $4.32 ¾ December corn chart gap fills, I do not have much hope unless we see a sizeable yield reduction that is unlikely.

There is potential for US new crop corn exports to yet be revised higher, but the large crop ahead may overshadow any such bullishness. The wheat market desperately needs a rally in corn, but until then and only up to then do I think wheat has a chance to rally. Once that corn chart gap fills, it’s probably time to sell wheat over the short-term. At the current pace of US negotiations with India as well as Russia and China, I wouldn’t count on any major orders or actions from those countries that would spur buying in the wheat market.

There were US soybean sales to “unknown” destination this week, which often means China, but it was not enough to excite the bulls with November soybean futures now down at the 200-day moving average at $10.26. Cash basis levels for soybeans continue to remain weak throughout the US with some elevators in the PNW stating they will not take soybeans that were not already contracted due to the lack of export options.

If you would like help in marketing your cash grain, Sidwell Solutions assists farmers in exactly that. We work with you to determine breakeven levels and monitor futures and cash basis bids to optimize your cash sales that align with your cash flow needs. If you are interested to have us on your team to help with cash grain sales, give us a call for program details and we will find the opportunities in the market to get your revenue above breakeven levels with a profit margin.

Sidwell Strategies is the one-stop shop to protect cattle with futures, puts, LRP or a combination of all, which is probably the best strategy overall. If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. He can be reached at (580) 232-2272 or at brady@sidwellstrategies.com. Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at https://www.sidwellstrategies.com/fccp-disclaimer-21951.