- Market Overview

- Futures

- Options

- Custom Charts

- Spread Charts

- Market Heat Maps

- Historical Data

- Stocks

- Real-Time Markets

- Site Register

- Mobile Website

- Trading Calendar

- Futures 101

- Commodity Symbols

- Real-Time Quotes

- CME Resource Center

- Farmer's Almanac

- USDA Reports

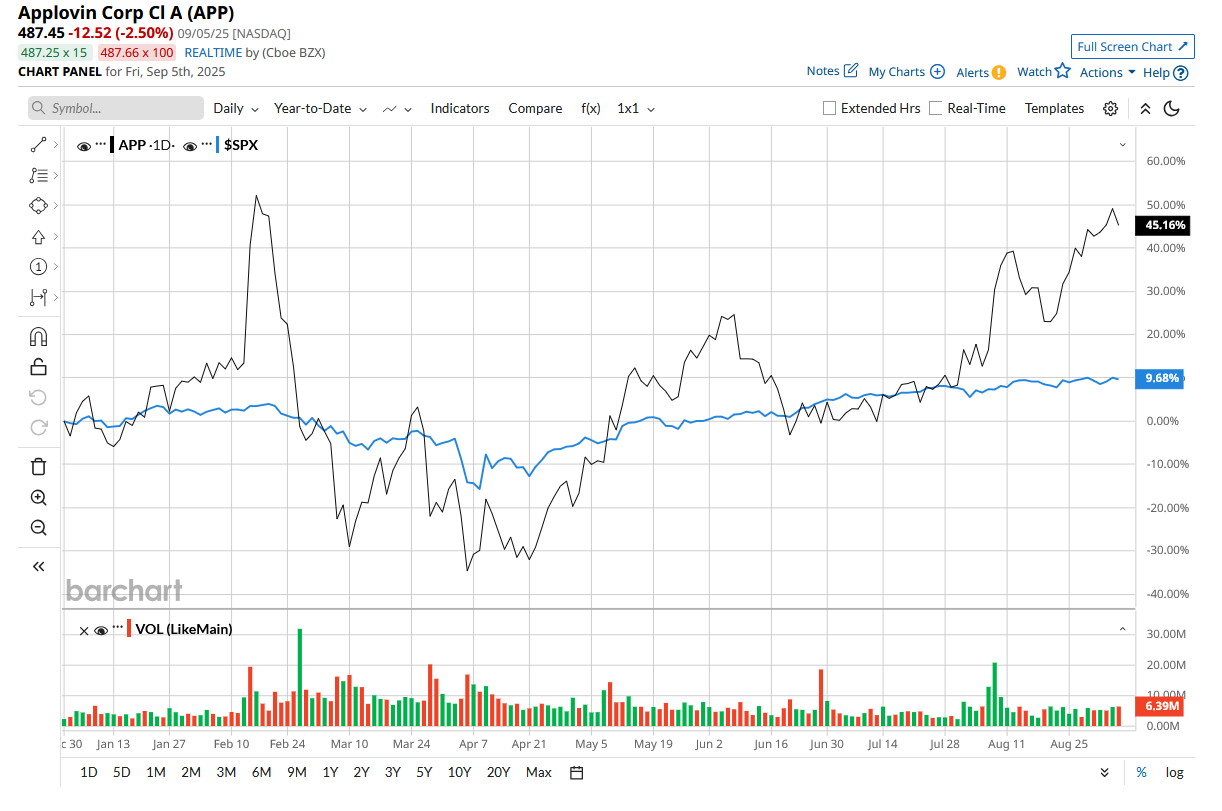

Up 50% in 2025, Is This ‘Strong Buy’ Growth Stock Worth Snapping Up Now?

AppLovin (APP) has long been recognized as a driving force in mobile gaming advertising, helping game developers scale efficiently. While gaming remains its core business, the company's recent second-quarter results indicate that something bigger is in the works. It is actively redirecting itself to become an improved e-commerce advertising platform.

APP stock, valued at $165 billion, is up an impressive 53% year-to-date (YTD), outperforming all the top tech titans in the “Magnificent Seven” group. Let us see if AppLovin can push this model and if now is a good time to buy APP stock.

AppLovin's Core Gaming Advertising Drove Growth in Q2

AppLovin is an advertising technology company that uses artificial intelligence (AI) to create technology and tools that enable advertisers to spend efficiently and publishers to monetize their apps, allowing both parties to grow profitably. It now even assists e-commerce businesses in acquiring new customers and increasing revenue. Its solutions include MAX, Adjust, Wurl, and SparkLabs, among others.

During the second-quarter earnings call, CEO Adam Foroughi stated that AppLovin's success remains rooted in its gaming advertising segment. Despite industry headwinds in app monetization, the company has consistently outperformed competitors thanks to its MAX marketplace, which is expanding at double-digit rates. This led to revenue surging an eye-catching 77% year-over-year (YoY) to $1.26 billion in Q2. Adjusted EBITDA (earnings before interest, tax, depreciation, and amortization) nearly doubled to $1.02 billion, representing an 81% margin. Net income rose 164% to $820 million.

Gaming's contribution is also not plateauing, according to Foroughi, who believes it is "going to get bigger." Management is confident that gaming will continue to drive 20% to 30% YoY growth. The sale of AppLovin's Apps business to Tripledot Studios generated $425 million in net cash, increasing the company's cash position to $1.2 billion at the end of the second quarter. The company also generated $768 million in free cash flow, which allowed it to repurchase $341 million worth of shares.

While gaming remains the core engine, AppLovin's expansion beyond that was the highlight of the quarter.

AXON Ads Manager: A Platform Built for the Next Decade

During the quarter, the company introduced AXON Ads Manager, AppLovin's new self-service portal for advertisers. CEO Adam Foroughi described it as the foundation for the company's next decade of expansion. AXON provides a variety of features, including direct control for marketers, credit card billing, automatically generated ads, and AI-powered campaign tools, among others.

While the company plans to open AXON Ads Manager on a referral basis beginning in October, a global public launch is scheduled for the first half of 2026. Once the platform is fully operational, the company plans to invest in paid marketing to attract advertisers, thereby initiating a new cycle of compounding growth.

The new e-commerce platform could help AppLovin expand its advertiser base beyond gaming. While e-commerce accounts for only 10% of AppLovin's revenue today, management believes that, if executed properly, e-commerce could eventually rival, if not outperform, its gaming segment. With continued gaming momentum and the rollout of AXON in Q4 and beyond, AppLovin remains optimistic about long-term growth in the coming quarters. The third quarter's revenue is expected to range between $1.32 billion and $1.34 billion. Adjusted EBITDA could range from $1.07 billion to $1.09 billion, with margins remaining at 81%.

Analysts who follow AppLovin predict exceptional growth over the next two years. For the full year, revenue is expected to rise 17.7% to $5.5 billion, followed by a 104% increase in earnings. Revenue and earnings are expected to grow by 27.7% and 40.4%, respectively, in 2026. APP stock is a little pricey now, trading at 37 times forward 2026 earnings estimates.

Is APP Stock a Buy on Wall Street?

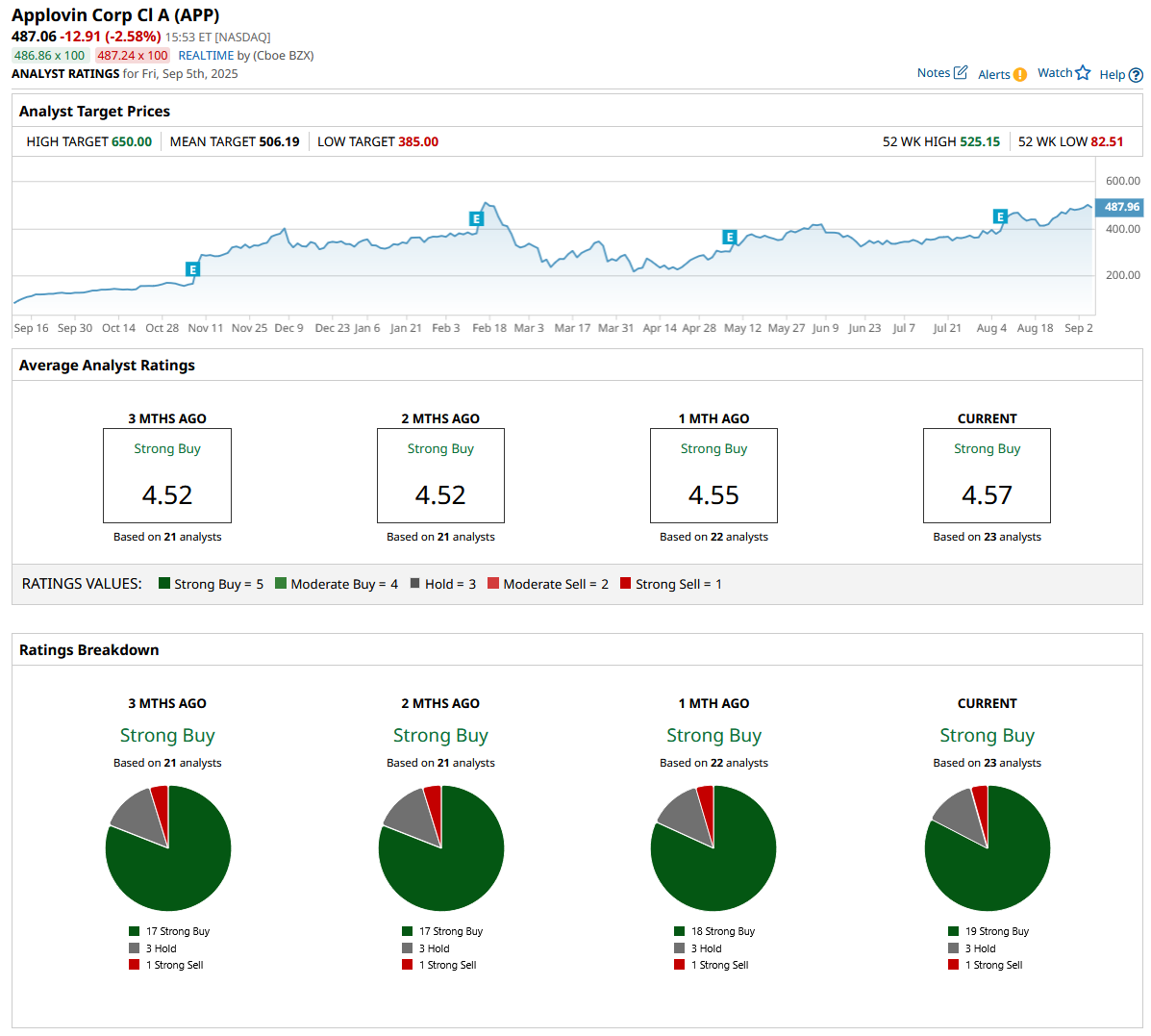

Wall Street analysts love APP stock, giving it an overall "Strong Buy" rating. Recently, Citi analyst Jason Bazinet initiated a “Buy” rating on AppLovin stock with a price target of $600. Bazinet believes that the planned expansion of its ad platform will significantly broaden AppLovin's customer base and revenue streams. He also identifies three catalysts that could boost the company's market position: "the upcoming eCommerce launch, the possibility of inclusion in the S&P 500 index, and the expected reduction in mobile gaming app store fees in 2026."

Out of the 23 analysts who cover the stock, 19 rate it as a “Strong Buy,” while three rate it as a “Hold” and one rates it a “Strong Sell.” The average target price of $506.19 suggests a 4% increase from current levels. Furthermore, the high price estimate of $650 implies that the stock could rally by up to 33.4% over the next 12 months.

AppLovin is executing flawlessly in its core gaming advertising segment while laying the groundwork for its next decade of growth with AXON. AppLovin is entering this new phase on a high note, with record revenue and margins, surging free cash flow, a streamlined balance sheet, and disciplined capital allocation. While this growth is a great long-term buy-and-hold opportunity, investors may want to wait for a better entry point.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.