- Market Overview

- Futures

- Options

- Custom Charts

- Spread Charts

- Market Heat Maps

- Historical Data

- Stocks

- Real-Time Markets

- Site Register

- Mobile Website

- Trading Calendar

- Futures 101

- Commodity Symbols

- Real-Time Quotes

- CME Resource Center

- Farmer's Almanac

- USDA Reports

Dear Google Stock Fans, Mark Your Calendars for July 23

/Alphabet%20Inc_%20and%20Google%20logos%20seen%20displayed%20on%20a%20smartphone%20by%20IgorGolovniov%20via%20Shutterstock.jpg)

Alphabet’s (GOOGL) Google has long been a pillar of strength in the tech world, powered by its hugely profitable Search business. Over the past decade, the stock has delivered a remarkable 452% return, reflecting years of steady growth and dominance. But lately, that growth narrative has hit some turbulence. This year, GOOGL stock has struggled to break out as concerns mount over the future of search in an artificial intelligence (AI) world.

For the first time since 2015, Google’s search engine market share has dipped below 90%, raising alarms among investors. Moreover, the rise of generative AI models — particularly OpenAI’s ChatGPT, where users get answers directly — has sparked fears that Google’s ad-based model could also lose its edge. Even so, Google isn’t standing still. The company is aggressively integrating AI across its ecosystem, aiming to revamp Search and future-proof its broader portfolio.

Beyond Search and ads, the company has a range of businesses — from cloud computing to hardware — that keep its fundamentals intact. So, with the tech giant’s second-quarter earnings just around the corner, here’s a closer look at GOOGL stock.

About Google Stock

Backed by multiple revenue streams, Google’s dominance is undoubtedly hard to ignore. The California-based company now operates across a broad digital spectrum, from cloud services and ad-based streaming to self-driving tech and healthcare innovation. In fact, Google was one of the early adopters of AI, well before it became a mainstream trend. It has since woven AI into much of its product ecosystem.

The company commands a hefty market capitalization of about $2.2 trillion. But despite its early strides in AI and long-standing dominance in tech, Google stock hasn’t kept up in 2025. Shares of GOOGL are down about 4% year-to-date (YTD), well behind both the tech-focused Nasdaq Composite Index's ($NASX) 7% gain and the broader S&P 500 Index's ($SPX) roughly 6% gain over the same period.

As questions swirl around Google’s ability to hold its ground in the fast-moving AI race, the tech giant is starting to look cheap. Currently trading at just 18.9 times forward earnings, Google’s price sits well below its own five-year average. The gap is even wider when compared to its “Magnificent Seven” peers, such as Microsoft (MSFT) at 33 times and Amazon (AMZN) at 36 times forward earnings. For a company with Google’s scale and reach, the current pricing stands out as a potential opportunity in an otherwise expensive tech landscape.

Google’s Q1 Earnings Snapshot

The tech giant opened fiscal 2025 on a strong note, with Q1 results released on April 24 comfortably surpassing analyst expectations. The company posted revenue of $90.2 billion, up 12% year-over-year (YOY) and ahead of the Street’s $89.2 billion forecast. Earnings stole the spotlight, coming in at $2.81 per share, a notable 49% jump from the prior year and an impressive 39% beat over consensus estimates.

The company’s core businesses continue to show resilience, suggesting that investors’ AI concerns may be overblown. Still the company’s crown jewel, Search generated $50.7 billion in revenue in the first quarter, up 9.8% YOY. Management pointed to strong engagement thanks to features like AI Overviews, which has reached more than 1.5 billion users monthly. Advertising revenue followed suit, climbing 8.5% annually to $66.9 billion.

On top of that, Google Cloud delivered standout growth, with revenue surging 28% to $12.3 billion, highlighting the company’s broad-based strength beyond just Search and ads. CEO Sundar Pichai highlighted a strong start to the year, crediting Google’s solid Q1 performance to broad-based momentum across the business. The CEO emphasized the company’s “full stack approach to AI" as a key driver of growth and pointed to the rollout of Gemini 2.5 as a major milestone.

Despite its aggressive push into AI, Google’s financials remain in excellent shape. The company closed the quarter with a hefty $95.3 billion in cash, cash equivalents, and marketable securities, along with $74.9 billion in free cash flow over the trailing 12 months. This strong cash engine allowed Google to return value to shareholders through $2.4 billion in dividends and a massive $15.1 billion in stock buybacks in Q1 alone.

Dear Google Stock Fans, Mark Your Calendars for July 23

With a major focus on AI advancements, during the company’s Q1 earnings call, management reiterated plans to invest approximately $75 billion in capital expenditures this year. Management noted that spending may fluctuate quarter to quarter due to shifts in delivery timelines and construction schedules. With a strong start to fiscal 2025 in Q1, management also signaled optimism ahead, stating that “Q2 will be even more exciting.”

The tech giant is gearing up to lift the curtain on its Q2 earnings results after the market closes on Wednesday, July 23. Ahead of this event, analysts are eyeing a 12.7% YOY bump in Q2 EPS to $2.13. Over the longer term, analysts project Google’s profit to improve by almost 19% annually to $9.56 per share in fiscal 2025, then grow another 7.9% to $10.32 per share in fiscal 2026.

What Do Analysts Expect for Google Stock?

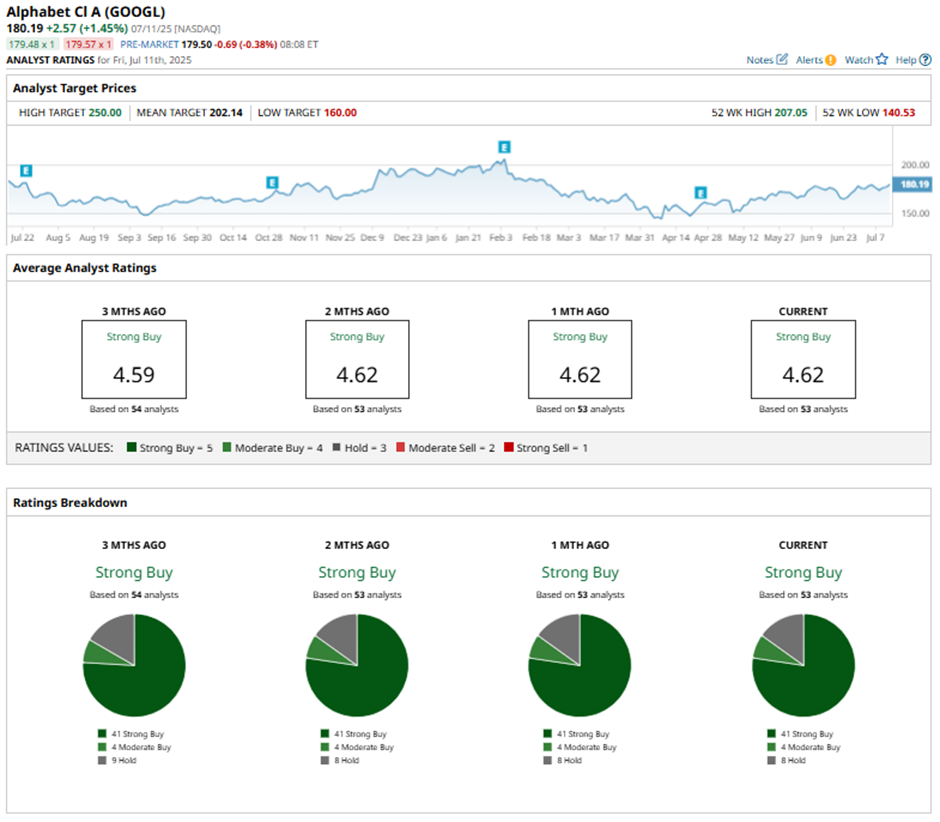

With Q2 results on the way, Wall Street is holding its bullish stance on GOOGL stock, with the consensus still leaning toward a “Strong Buy” rating overall. Of the 53 analysts offering recommendations, a majority of 41 analysts advocate a “Strong Buy,” four give a “Moderate Buy,” and the remaining eight suggest a “Hold" rating. The average analyst price target of $202.14 represents potential upside of 11%, while the Street-high target of $250 implies a 37% rally from current levels.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.